Exploring Unsecured Loans: Types and Advantages Explained

Delving into the realm of unsecured loans unveils a variety of options tailored to diverse financial needs. Unlike secured loans requiring collateral, unsecured loans offer flexibility without risking assets. Understanding the types and advantages of unsecured loans provides insight into accessible financial solutions for personal and business endeavors. From credit cards to personal lines of credit, this exploration elucidates the nuances and benefits of unsecured lending, empowering individuals and businesses to make informed borrowing decisions suited to their circumstances and goals.

What is an Unsecured Loan?

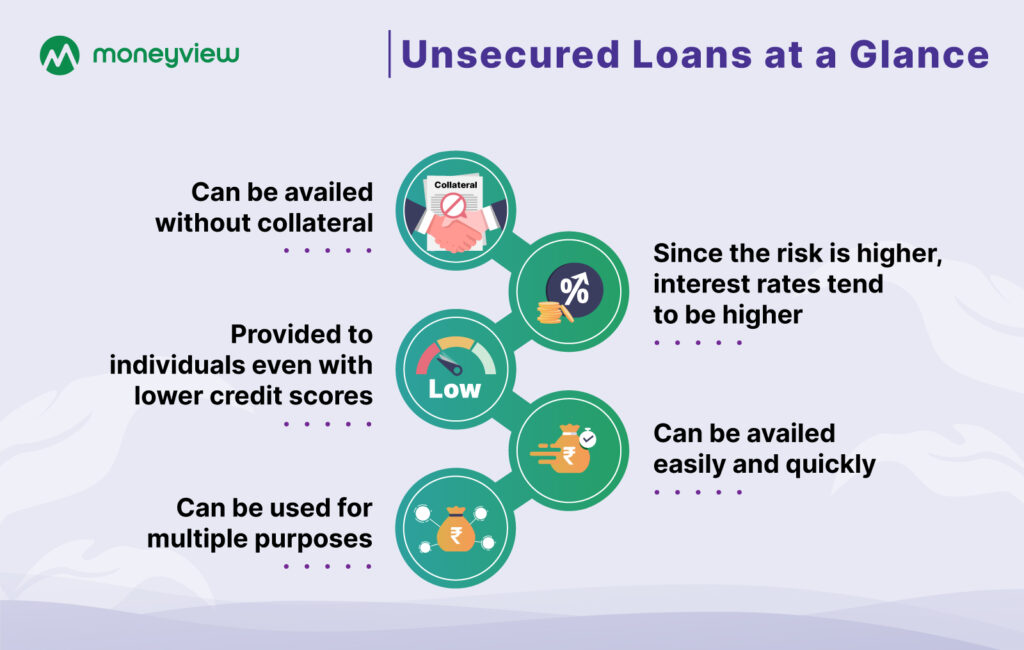

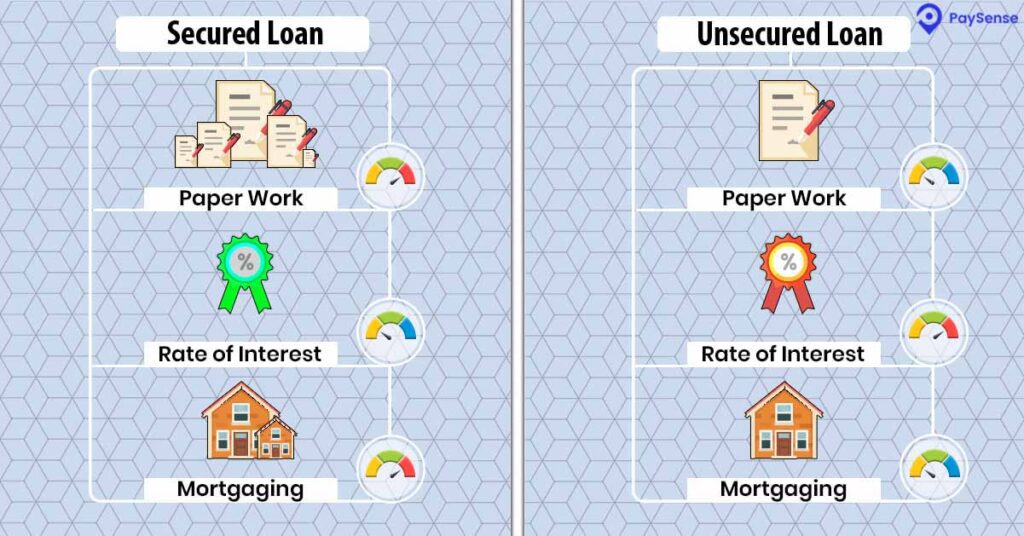

An unsecured loan is a type of loan that you can get without having to offer any assets as security to the bank or NBFC. Instead, they approve it based on things like your credit score, stable income, and ability to repay. Since lenders face more risk with these loans, they usually charge higher interest rates than secured loans. Your credit score is also crucial—if it’s low, getting an unsecured loan might be tough, so it’s important to work on improving it. Now, let’s look at the various types of unsecured loans.

Unsecured Loans Types

Lenders offer various types of unsecured loans to meet different financial needs. Here are some common ones:

- Signature Loan: Also known as good-faith loans, signature loans only require your promise to repay, without needing any collateral. They’re based on your creditworthiness and ability to repay. Sometimes, a co-signer may be required for added security. These loans can be used for anything, like consolidating debt or covering personal expenses. They often have fixed interest rates, making monthly payments predictable.

- Personal Loan: Popular among individuals, personal loans are versatile and have no specific end-use restrictions. They’re approved based on factors like your creditworthiness, income stability, and repayment capacity. Typically, they have fixed interest rates and repayment periods of up to 60 months. Having a good credit score and steady income can lead to better interest rates.

- Peer-2-Peer Loans: Peer-to-peer loans, or P2P lending, connect individuals who want to borrow with those willing to lend through online platforms. They’re regulated but not like banks or NBFCs. Interest rates may be higher, and approval depends on factors like credit risk. These loans offer flexibility and may have fewer eligibility requirements compared to traditional loans.

- Instant Loans: Instant loans provide quick access to funds, often within hours of application. They’re designed for urgent expenses and have shorter repayment periods. Because of the convenience and speed, interest rates may be higher, and loan amounts are usually small to moderate.

- Line of Credit: A line of credit gives you a set credit limit that you can borrow against as needed. You can access funds and repay them at your convenience, with a variable interest rate. However, eligibility requirements are strict, often requiring an excellent credit history and financial status.

How Unsecured Loans Work?

An unsecured loan doesn’t require collateral like a house or car to secure it. Instead, lenders assess the applicant’s creditworthiness, financial history, income, and repayment capacity. Here’s how it works:

- Application: The individual applies for the loan by filling out an application form provided by the lender.

- Credit Check: Lenders review the applicant’s credit score to assess the risk of lending. Higher credit scores are usually preferred for unsecured loans.

- Loan Approval: If the applicant meets creditworthiness criteria, the lender evaluates their income and repayment capacity. Based on this, they decide whether to approve or reject the application.

- Loan Terms: Once approved, the lender sets the loan terms, including interest rates, repayment terms, tenure, and associated fees. The applicant reviews and agrees to these terms.

- Loan Disbursal: After signing the agreement, the lender deposits the funds into the borrower’s bank account.

- Repayment: Repayment begins the following month, with Equated Monthly Installments (EMIs) covering principal and interest. Payments must be made according to the agreed schedule.

What are the Features of Unsecured Loan?

Unsecured loans offer several distinctive features:

- No Collateral Requirements: Unlike secured loans, unsecured loans don’t require collateral. Borrowers don’t have to risk their assets to qualify for these loans.

- Credit-based Approval: Lenders assess applicants based on their credit score, credit history, and financial behavior. A good credit score and responsible financial habits increase the likelihood of loan approval.

- Fixed Interest Rate: Unsecured loans typically come with fixed interest rates throughout the loan term. This stability makes it easier for borrowers to budget and plan their finances.

- Short to Medium Loan Tenure: Unsecured loans often have shorter repayment periods compared to secured loans. For example, personal loans typically range from 12 to 60 months, providing borrowers with flexibility in repayment.

- Flexible Use of Funds: Lenders impose no restrictions on how borrowers use the loan amount. Funds can be utilized for various purposes, including debt consolidation, medical expenses, home improvements, and more.

- Quick Approval: Unsecured loan applications can be completed online, and approval decisions are often made swiftly. Some lenders offer same-day funding or disbursal within a few days, providing borrowers with quick access to funds when needed.

Unsecured Loan- Advantages and Disadvantages

Unsecured loans offer various benefits, but they also come with some drawbacks:

Benefits:

- No Collateral Required: There’s no need to offer assets as collateral, reducing the risk of asset loss if repayments are missed.

- Flexible Use of Funds: Unlike specific-purpose loans, unsecured loan funds can be utilized for any need.

- Quick Access to Funds: Approval and disbursal are faster compared to secured loans, providing timely financial assistance.

- Minimal Documentation: The application process is simplified, requiring only basic documents for verification.

- Accessible to a Wide Range of Borrowers: Individuals with diverse credit profiles can access unsecured loans, albeit with varying interest rates.

Disadvantages:

- Higher Interest Rates: Lenders charge higher interest rates due to the increased risk of default.

- Limited Loan Amount: The loan amount is determined by income and financial status, potentially restricting borrowing capacity.

- Shorter Loan Terms: Repayment periods are shorter, leading to higher monthly payments and budget strain.

- Limited Negotiation Power: Borrowers have less leverage in negotiating terms compared to secured loans.

- Risk of High Debt Levels: Easy accessibility may lead to overborrowing, resulting in financial strain and reduced savings.

Unsecured loans offer borrowers flexibility and convenience without the need for collateral. With features like quick approval, fixed interest rates, and flexible usage of funds, they provide valuable financial solutions for various needs. However, it’s essential for borrowers to maintain a good credit score and responsible financial behavior to increase their chances of approval and ensure successful repayment. Like this post? Don’t forget to check out our other tips and stories in our Latest section